Why I Picked Up UPS And Left FedEx By The Curb

With the ubiquity of the e-commerce sector all but sealed, I decided that my retirement portfolio needed some skin in this game. I compared the two largest players responsible for transferring packages from the Interwebs to front doorsteps, with the end result being I have added United Parcel Service (NYSE:UPS) to my holdings as opposed to Federal Express (NYSE:FDX).

History is a Good Barometer, Kinda

While it is true that "past performance is not a guarantee of future results," I could easily make the argument that when it comes to comparisons, the importance of a previous track record is directly correlative to how long one intends to hold the position. To channel our Dear Leader, winners tend to keep winning. And since this newly-opened position is in a retirement portfolio that has a multi-decade time horizon, I would maintain that what has happened in the not-so-distant past is imperative.

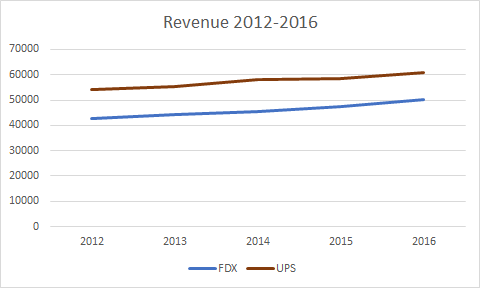

To look at a growth in revenues over the past five years:

It can be seen that FedEx over this time has increased its revenues by 18%, compared to UPS's 12.5%. However, even if this trend were to continue for the foreseeable future, it will be years before it matters.

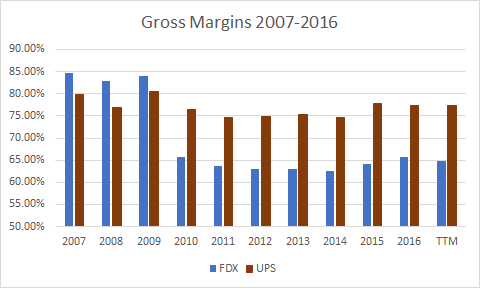

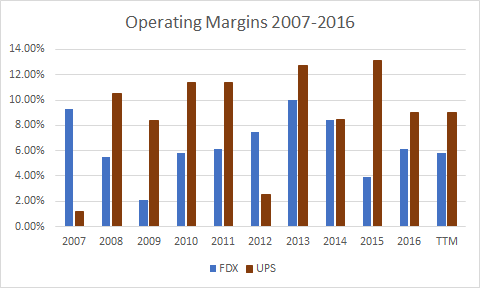

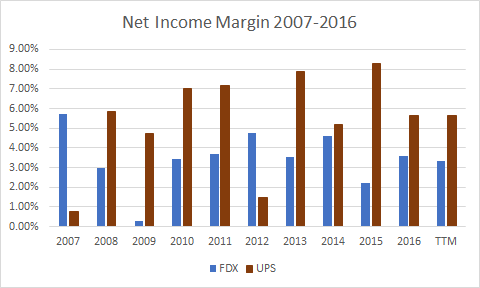

The answer is margins. To borrow an analogy I have used previously from the racetrack, what matters as much as if not more than horsepower in the engine is the amount of that horsepower that actually makes it to the wheels. Conceivably, a car with a more powerful engine could be slower than a weaker competitor due to inefficiencies within its engine. However, in the UPS vs. FedEx race, not only does UPS have a more powerful engine (revenues), more of that horsepower gets to the wheels (margins).

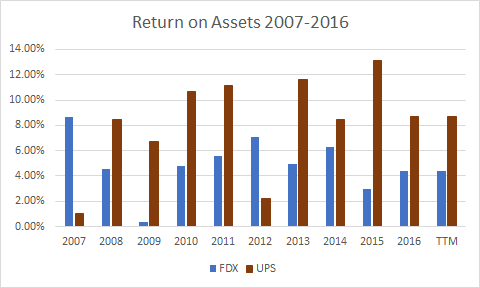

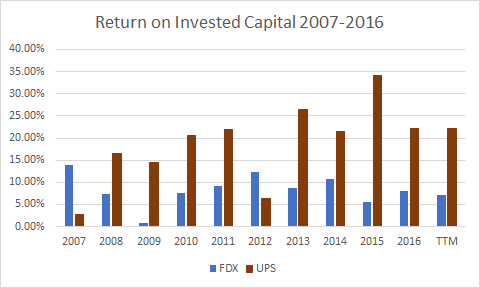

As a case in point, except for hiccups in 2007 and 2012, UPS has beaten FedEx in every conceivable important metric every year for the last decade:

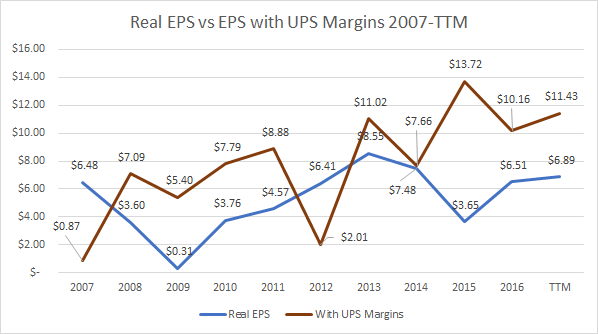

On the surface, this appears inconsequential. However, the difference amounts to billions of dollars. To put this in very real terms, here is a chart of what FedEx's EPS was from 2007 to 2016, versus what they could have been had FedEx had UPS's margins in those years:

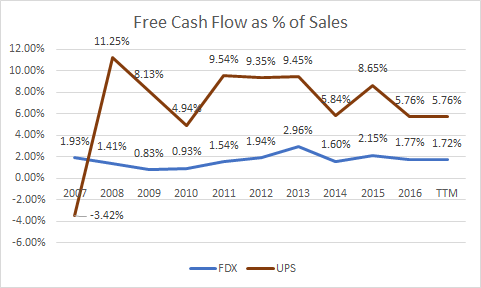

For the dividend investors among us, the superiority of UPS's margins have a direct correlation to how much free cash flow is available to possibly reserve for dividends:

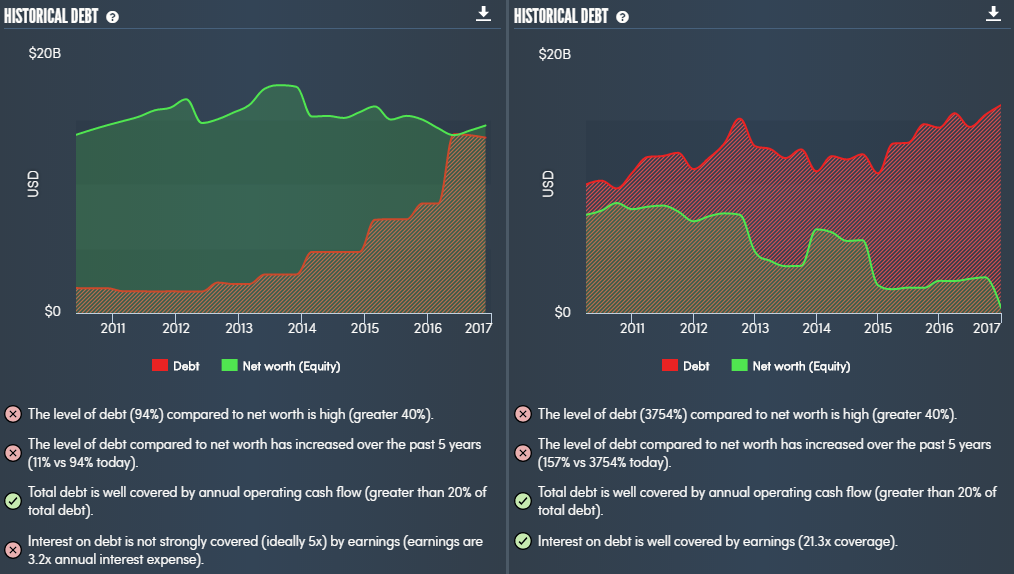

Though at first glance, the debt picture at UPS looks considerably worse than that at FedEx on an equity basis (with help from a Simply Wall St infographic), there are two things to consider.

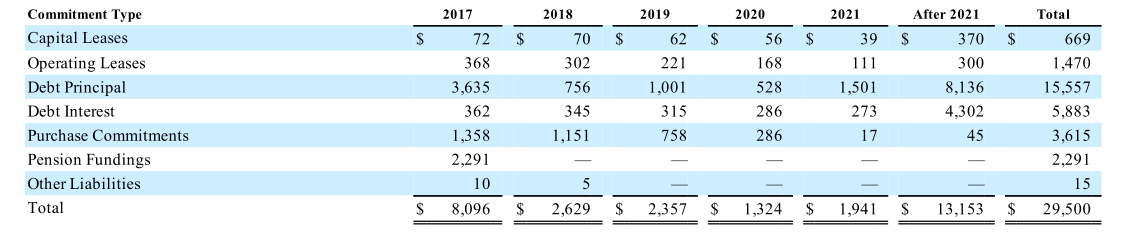

First, as seen above, FedEx's earnings only represent 3.2x its annual interest expense, while at UPS the number is over 21x. Secondly, though UPS's debt principal on the books is over $15 billion at this point, after 2017, there are no comparatively major liabilities until 2021.

My investment in UPS is proof-positive that I think that the management of bottom lines in Atlanta, GA is more than adequate enough to handle the debt issues. And as a prospective owner of the business, I am entitled to a portion of that bottom line, whether that be in the form of dividends or retained earnings plowed back into the business. Given the above data, I can make no other conclusion than that my interests as a UPS shareholder would be better taken care of than if I was a shareholder of FedEx.

Growth Prospects

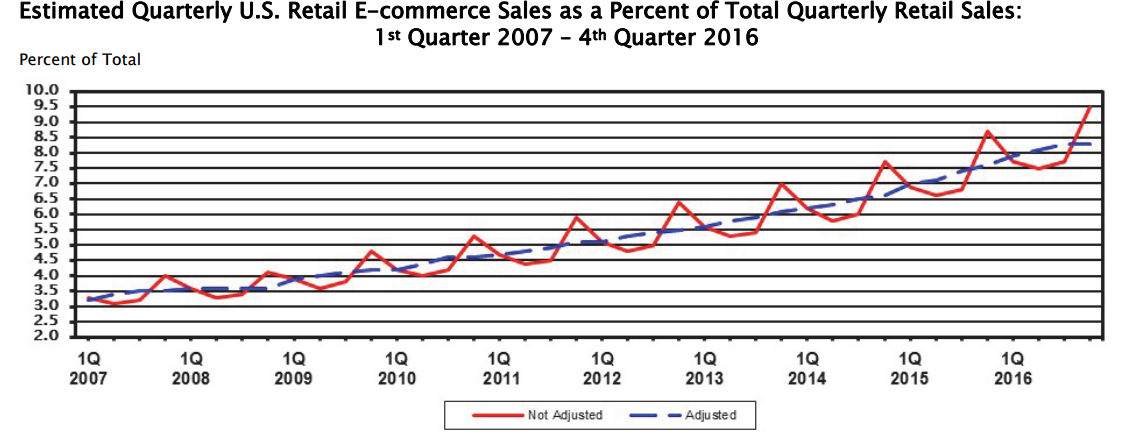

There are two main growth drivers for both UPS and FedEx. The elephant in the room is the growth of e-commerce. According to the US Census Bureau and the casual observer, e-commerce is accounting for a greater percentage of total retail sales with FedEx estimating that volumes will double by 2020. With this in play, there is a prodigious and obvious opportunity for both FedEx and UPS to have a growth driver for years to come.

Recently, the behemoth Amazon (NASDAQ:AMZN) has made motions towards taking on more of the delivery of packages themselves. With them spending over $11 billion annually in shipping, the idea of taking on more of that burden is certainly attractive. With an estimated savings of $3 per package, if it handled more of the delivery, the savings would add up quickly.

Surprisingly though, the threat this poses for both FedEx and UPS is rather muted. Moody's estimates that Amazon spent $665 million with FedEx and $2.2 billion with UPS in 2015 - inconsequential when compared to revenues of $47.4 billion and $58.3 billion, respectively.

The second growth driver for FedEx and UPS would be acquisitions. In yet another exhibit of government bureaucracy, the fact that the European Union just this week overturned a 2013 decision blocking the merger between UPS and TNT Express (OTC:TNTEF) must have served as salt in an open wound, especially since this paved the way for the FedEx and TNT merger. Perhaps, UPS could ask the EU to reimburse them for the $284 million break-up fee.

This sector of the market is dominated by UPS and FedEx, with the rest of the market highly fragmented downstream. It's possible that with TNT now off the table, the only other meaningful in-kind acquisition would be DHL. Surely the prospect of it also being swallowed up would be seen as too much of a duopoly in the eyes of regulators.

Having been kicked in the groin by Brussels, UPS has recently cast its acquisitive eye towards the third-party logistics market with its purchase of Coyote Logistics, and healthcare logistics with its acquisition of Marken. Personally, I would love to see them take a sniff in the direction of C.H. Robinson Worldwide (NASDAQ:CHRW), but it's nothing more than conjecture on my part.

Income Potential

FedEx's recent dividend growth has been absolutely astounding. The fact that it pays $1.60 per share annually these days is amazing since in just 2011 the dividend was less than one-third of that. And with acquisition targets becoming harder and harder to come by, logic would dictate that more cash could be used by FedEx in the future for dividends and share buybacks.

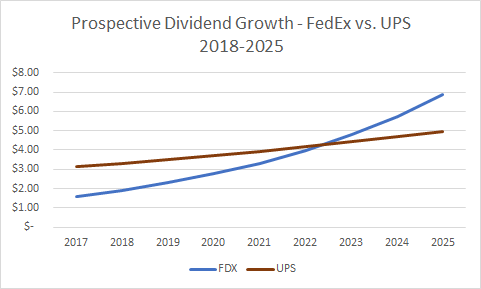

For strictly dividend growth, however, FedEx's recent prodigious growth won't mean much by way of comparisons with UPS immediately. It wasn't too long ago that Dividend House showed that stocks with higher dividend growth but a lower starting rate may not be all they are cracked up to be, when compared with their higher-starting but slower-growing brethren.

Specifically to the FedEx vs. UPS comparison, if FedEx was able to keep a 20% growth compared with a hypothetical 6% growth rate for UPS, the per-share comparison would not reverse until 2023:

Given this fact coupled with my time horizon, it would seem that I should prefer FedEx's prospects. However, there are two main reasons why I don't. The first has everything to do with the margin discussion above. Secondly, FedEx as recently as 2001 didn't pay a dividend at all, while UPS has either increased or maintained a dividend since 1970, almost a full thirty years before it even became a public company.

Valuation

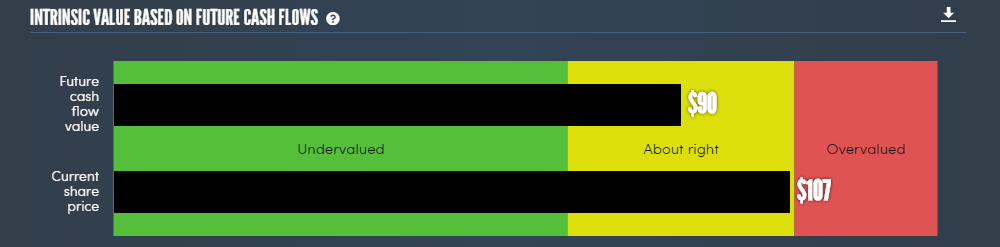

At my purchase price of $106.90 on 2/21, I locked in a 3.1% yield and while that's not hideous, it's not much of a bargain, either:

Fair value over at S&P Capital IQ is $107.30, with Morningstar coming in at $102 and a discounted cash flow analysis infographic over at Simply Wall St shows I just barely purchased it within an acceptable range.

Optimally, I would love to get about an 8-10% margin of safety from these numbers, which would be a range of roughly $94-$96. It could happen, but I really do not expect it to imminently given the current environment. If this were in a taxable account, I would probably wait to see what happens. But since this is in a retirement account with a not-quite-thirty-year time horizon, I figure I have a while to fix any valuation mistakes I might have made, if time does not do it by itself.

Summary

Yes, FedEx's earnings growth is expected to outpace that of UPS. And if all I was concerned about was price appreciation, I would choose FedEx over UPS. However, for the income-minded investor who is looking to take a bite into this sector, there really is no comparison. Pick up UPS and leave FedEx at the curb.

Disclosure: I am/we are long UPS.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it . I have no business relationship with any company whose stock is mentioned in this article.

Comments

Post a Comment